CRS Report for Congress

Social Security: Raising the Retirement Age

Background and Issues

Geoffrey Kollmann

Domestic Social Policy Division

Summary

The Social Security “full retirement age” — the age at which retired workers, aged

spouses, or surviving aged spouses receive benefits that are not reduced for “early”

retirement — will gradually rise from 65 to 67 beginning with people who attain age 62

in 2000 (i.e., those born in 1938). Early retirement benefits will still be available

beginning at age 62 (age 60 for aged widows and widowers), but at lower levels.

To help solve Social Security’s long-range financing problems, it has been

proposed that these ages be raised further. Bills introduced in the last five Congresses

would, among other things, accelerate the phase-in of the increase in the full retirement

age to 67, raise the early retirement age to 65 or 67, and raise the full retirement age to

69 or 70. This report will be updated to reflect any legislative developments.

CRS-2

bolstering the financing of the program. It also was argued that it would properly

recognize the substantial increases in longevity that had occurred and were projected to

continue.

Raising the full retirement age to 67. When Congress enacted legislation in

1983 (P.L. 98-21) to solve Social Security’s financing problems, it included a provision

that gradually will raise the full retirement age (the age at which one receives unreduced

benefits) from age 65 to age 67. It does so in two steps. First, the full retirement age

(FRA) will increase by 2 months for each year that a person is born after 1937 (i.e., attains

age 62 after 1999), until it reaches age 66 for those who were born in 1943 (who attain

age 62 in 2005). Second, it will increase again by 2 months for each year that a person

is born after 1954 (i.e., attains age 62 after 2016), until it reaches age 67 for those who

were born after 1959 (who attain age 62 after 2021). Early retirement still will be

available, but benefits will be lower, e.g., the actuarial reduction in retirement benefits

ultimately will be 30%, instead of the present 20%, at age 62. The age for full benefits

for aged spouses and widow(er)s likewise will rise to 67.

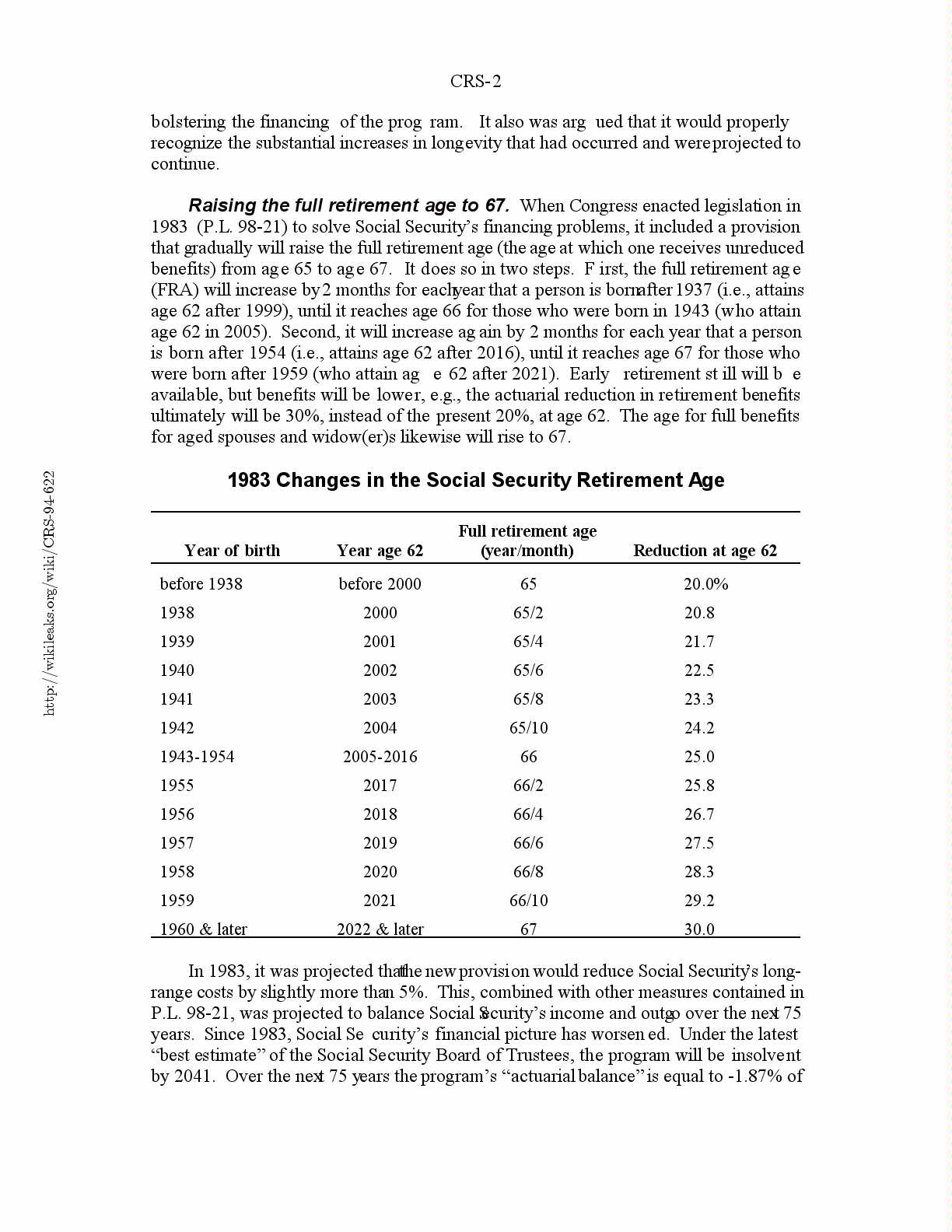

1983 Changes in the Social Security Retirement Age

Full retirement age

Year of birthYear age 62(year/month)Reduction at age 62

before 1938before 20006520.0%

1938 2000 65/2 20.8

1939 2001 65/4 21.7

1940 2002 65/6 22.5

1941 2003 65/8 23.3

1942 2004 65/10 24.2

1943-1954 2005-2016 66 25.0

1955 2017 66/2 25.8

1956 2018 66/4 26.7

1957 2019 66/6 27.5

1958 2020 66/8 28.3

1959 2021 66/10 29.2

1960 & later2022 & later6730.0

In 1983, it was projected that the new provision would reduce Social Security’s long-

range costs by slightly more than 5%. This, combined with other measures contained in

P.L. 98-21, was projected to balance Social Security’s income and outgo over the next 75

years. Since 1983, Social Security’s financial picture has worsened. Under the latest

“best estimate” of the Social Security Board of Trustees, the program will be insolvent

by 2041. Over the next 75 years the program’s “actuarial balance” is equal to -1.87% of

View Page Image

CRS-3

taxable earnings.1 Said another way, the program’s expenditures are projected to exceed

its income by 14%. Combined with growing concern about the cost of “entitlement”

programs generally, this long-range problem has renewed interest in examining changes

in the retirement age.

Arguments For Raising the Retirement Age

Advocates of raising the retirement age point out that life expectancy has improved

significantly since Social Security was enacted. When benefits were first paid in 1940,

a 65-year-old on average lived about 13 more years. In 2002, a 65-year-old is expected

to live about 18 more years, and it is projected that by 2030 a 65-year-old will live 20

more years. They cite these longevity increases, as well as improvements in the health

of the elderly, as a reasonable basis for encouraging workers to retire later. Also, they

highlight the savings it would produce. According to the Social Security Administration,

raising the FRA to 70 in 2029 would reduce long-range costs by about 6%.

Proponents of raising the retirement age say that it is an equitable way to control the

program’s costs, because it would give the people affected time to adjust their retirement

plans. They contrast this with cuts in benefits for current retirees, such as restraints on

cost of living increases, that would impose the burden on elderly people who have few

options for offsetting their losses. It is argued that current workers would probably prefer

a change in the retirement age, to which they could adjust by lengthening their work

careers or by increasing savings to supplement Social Security, to an increase in their

Social Security taxes. Proponents portray raising the retirement age as unlike a benefit

cut, because full benefits still would be payable — people just would receive them later.

Arguments Against Raising the Retirement Age

Opponents of raising the retirement age say that it is simply a cut in benefits, which

would unfairly penalize workers who planned their retirement based on current law. They

aver that the burden would be concentrated on those unable to work until later ages

because they are unemployed or work in arduous occupations. They maintain it would

adversely affect those racial minorities that have relatively shorter life spans. They

dispute that increased longevity necessarily corresponds with ability to work at later ages

— people may be living longer, but with more chronic illnesses and impairments.

Opponents also disagree that it would be better to place the burden on current workers

rather than current recipients. They point out that today’s retirees receive a better deal

from the program than will today’s workers. For example, a person who earned average

wages and who retires at age 65 in 2000 recovers the value of the retirement portion of

1 Taxable earnings is the amount of wages or self-employment income that are subject to the

Social Security tax. For long-range forecasting, Social Security’s income and costs are expressed

as a percentage of taxable earnings. Measuring the program’s income and outgo over long

periods (75 years) by describing what portion of taxable earnings they represent is more

meaningful than using dollar amounts, because the value of the dollar changes over time. The

system’s long-range costs and income are projected to be 15.59% and 13.72% of taxable

earnings, respectively, a difference of 14%. To restore actuarial balance, revenues would have

to be raised and/or outgo reduced by the equivalent of 1.87% (15.59-13.72) of taxable earnings.

View Page Image

CRS-4

his and his employer’s Social Security taxes plus interest in 17 years — this payback time

expands to 21 years for a similar individual retiring in 2020. Also, as Social Security is

subject to the income tax only if a recipient’s income is above certain thresholds, the

benefits of 68% of current recipients are exempt from taxation. As these thresholds are

not indexed, it is projected that eventually inflation will cause virtually all future Social

Security recipients to pay tax on their benefits. Furthermore, opponents maintain that it

would not necessarily be burdensome to ask current retirees to share in cutting costs,

especially if the measures are targeted on those with higher incomes.

Finally, opponents contend that raising the retirement age would raise costs for the

Social Security disability program. First, it could increase the incentive for elderly

workers to apply for disability rather than wait to attain a more distant retirement age.

Second, if early retirement benefits were still available at age 62, but subject to higher2

actuarial reductions, they would become less attractive compared to disability benefits.

(For more about raising the retirement age, see GAO report Social Security Reform:

Implications of Raising the Retirement Age, HEHS-99-112, August 1999. For more about

changing the early retirement age, see CRS Report RL30558, Social Security: A

Discussion of Some Issues Affecting the Early Retirement Age, by Geoffrey Kollmann.

Proposals and Options

Legislative Proposals in the 104th Congress

S. 825 (Kerrey). Raised the FRA by 2 months per year that a person was born after

1937 (who attain age 62 after 1999), until it reached age 70 for those born in 1967 (who

attain age 62 in 2029) or later. Also raised the early retirement age in tandem, reaching

age 65 for persons born after 1954. For those born after 1967, the full and early

retirement ages would increase by 1 month for every 2 years.

H.R. 3758 (N. Smith). Raised the FRA by 3 months per year that a person is born

after 1937, reaching age 69 for those born in 1953. The early retirement age would have

risen by 3 months per year, reaching age 65 for those born in 1949. The earliest age for

widow(er) benefits likewise would have risen, to age 63 for those born in 1949. After

2015, the FRA would have been adjusted so as to maintain a constant ratio of projected

life expectancy at the FRA to potential working years, and the early retirement age would

have been adjusted to be 4 years (6 years for widow(ers)) lower than the FRA.

2 Disability benefits are computed similarly to retirement benefits, but are calculated as if the

worker attained the full retirement age in the year he or she became disabled. Thus, if a worker

between the ages for early retirement and full retirement can qualify for disability, the disability

benefit can be significantly greater than the actuarially reduced retirement benefit. For example,

if a worker today could qualify for disability at age 62, his or her benefit would be 26% higher

than if he or she received early retirement benefits. For people whose full retirement age will be

67, this difference would grow to 43%.

CRS-5

Proposals by the 1994-1996 Advisory Council on Social Security

In January 1997, the last Advisory Council on Social Security3 issued a report on

recommendations to solve Social Security’s long-range financial problems. Although it

split into three factions because it could not agree on a single set of proposals, two of the

factions recommended that the increase in the FRA to 67 in current law be accelerated,

so that it would be fully effective in 2016 (instead of 2027), and indexed thereafter to

increases in longevity. One of these two factions also recommended that the early

retirement age be raised in tandem with the FRA until it reached age 65, where it would

remain, but with increased actuarial reductions as the FRA continues to increase.

Legislative Proposals in the 105th Congress

S. 321 (Gregg). Raised the FRA and the early retirement age to 70 and 65,

respectively, by 2037, and by one-half month per year thereafter.

H.R. 2768 (Sanford). Raised the FRA to 70 by 2037 in the same manner as S. 825

in the 104th Congress.

H.R. 2782 (Sanford). Raised the FRA to age 70 by 2037, and the early retirement

age to 65 by 2020, both increasing by one-half month per year thereafter.

H.R. 2929 (Porter). Raised the FRA in the same manner as H.R. 2768.

H.R. 3082 (N. Smith). This bill would have raised the full retirement and earlyth

retirement ages in the same manner as H.R. 3758 in the 104 Congress.

S. 1972 (Moynihan). This bill would have raised the FRA to 68 by 2017, and

would have raised it thereafter by 1 month every 2 years until it reached age 70.

S. 2313 (Gregg) and H.R 4256 (Kolbe).. Raised the FRA to 70 by 2037 in the

same manner as S. 321, but would have increased it thereafter by one-third month a year.

Legislative Proposals in the 106th Congress

H.R. 251 (Sanford).. Raised the FRA by 2 months per year that a person was

born after 1937, reaching age 70 for those born in 1967, and thereafter by 1 month every

2 years. The early retirement age likewise would have risen, reaching age 65 for those

born in 1954, and again beginning with those born in 1968 by 1 month every 2 years.

3 The Social Security Act used to require that every 4 years the Secretary of Health and Human

Services appoint an Advisory Council on the Status of the Social Security program. However,

P.L. 103-296, which made the Social Security Administration independent in 1995, created a

permanent Advisory Board and abolished future Advisory Councils.

View Page Image

CRS-6

H.R. 874 (Porter, et al.). Raised the FRA by 2 months for each year that a person

was born after 1937, until it reaches age 70 for those born in 1967 or later. Gradually

increased the reduction for early retirement, reaching 53% for persons born after 1966.

H.R. 1793 (Kolbe/Stenholm). Raised the FRA by 2 months per year for persons

born from 1938 to 1949, and increased early and full retirement ages by ½ month per year

thereafter. From 2001 to 2005, gradually increased the actuarial reduction for persons

retiring at the early retirement age, reaching 37% for persons born in 1943 and later.

H.R. 3206 (N. Smith). Raised the FRA by 2 months per year for persons born

from 1938 to 1949, and increased it by ½ month per year thereafter.

S. 21(Moynihan). This bill would have restored the FRA to 65.

S. 1383 (Gregg, et al.). Similar to H.R. 1793, but did not change the early

retirement age, and the increase in the reduction for early retirement began in 2000.

Legislative Proposals in the 107th Congress

H.R. 2771 (Kolbe/Stenholm). Accelerates the increase in the FRA so that it reaches

67 for persons born in 1949 and later, and increases the actuarial reduction for early

retirement benefits, reaching 37% for persons born in 1944 and later.

Financial Effects of Proposals to Raise the Retirement Age

The Social Security Administration has prepared the following estimates of the effect

(expressed in percent of taxable earnings) of other variations of raising the FRA. In each

instance, the age is increased by 2 months each year after 1999, and early retirement

remains at age 62 for retirees and aged spouses and age 60 for aged widow(er)s.4

Appropriate actuarial reductions for early retirement are made under each proposal.

Effect of Alternative Proposals to Raise the Full Retirement Age

Reduction at age

Full retirement ageYear fully effective62Long-range effect

67 2027 30.0% ——

{kind=link}

{kind=link}

{kind=link}