Social Security: The Cost-of-Living

Adjustment in January 2009

Gary Sidor

Information Research Specialist

Knowledge Services Group

Summary

To compensate for the effects of inflation, Social Security recipients receive a cost-

of-living adjustment (COLA) in January of each year. The Consumer Price Index for

Urban Wage Earners and Clerical Workers (CPI-W), updated monthly by the

Department of Labor’s Bureau of Labor Statistics (BLS), is the measure used to compute

the change. The Social Security COLA is based on the percentage change in the average

CPI-W for the third calendar quarter of the previous year to the third calendar quarter

of the current year. The COLA becomes effective in December of the current year and

is payable in January of the following year (Social Security payments always reflect the

benefits due for the preceding month).

The 5.8% COLA payable in January 2009 was triggered by the rise in the CPI-W

from the third quarter of 2007 to the third quarter of 2008. This COLA triggers identical

percentage increases in Supplemental Security Income (SSI), veterans’ pensions, and

railroad retirement benefits, and causes other changes in the Social Security program.

Although COLAs under the federal Civil Service Retirement System (CSRS) and the

federal military retirement program are not triggered by the Social Security COLA, these

programs use the same measuring period and formula for computing their COLAs.

Their recipients will also receive a 5.8% COLA in January 2009. This report is updated

annually.

How the Social Security COLA Is Determined

An automatic Social Security benefit increase reflects the rise in the cost of living

over roughly a one-year period. The CPI-W, updated monthly by the BLS, is the measure

used to compute the change. The Social Security COLA is based on the percentage

change in the average CPI-W for the third calendar quarter of the previous year to the

third calendar quarter of the current year. The COLA becomes effective in December of

the current year and is payable in January of the following year (Social Security payments

always reflect the benefits due for the preceding month).

View Page Image

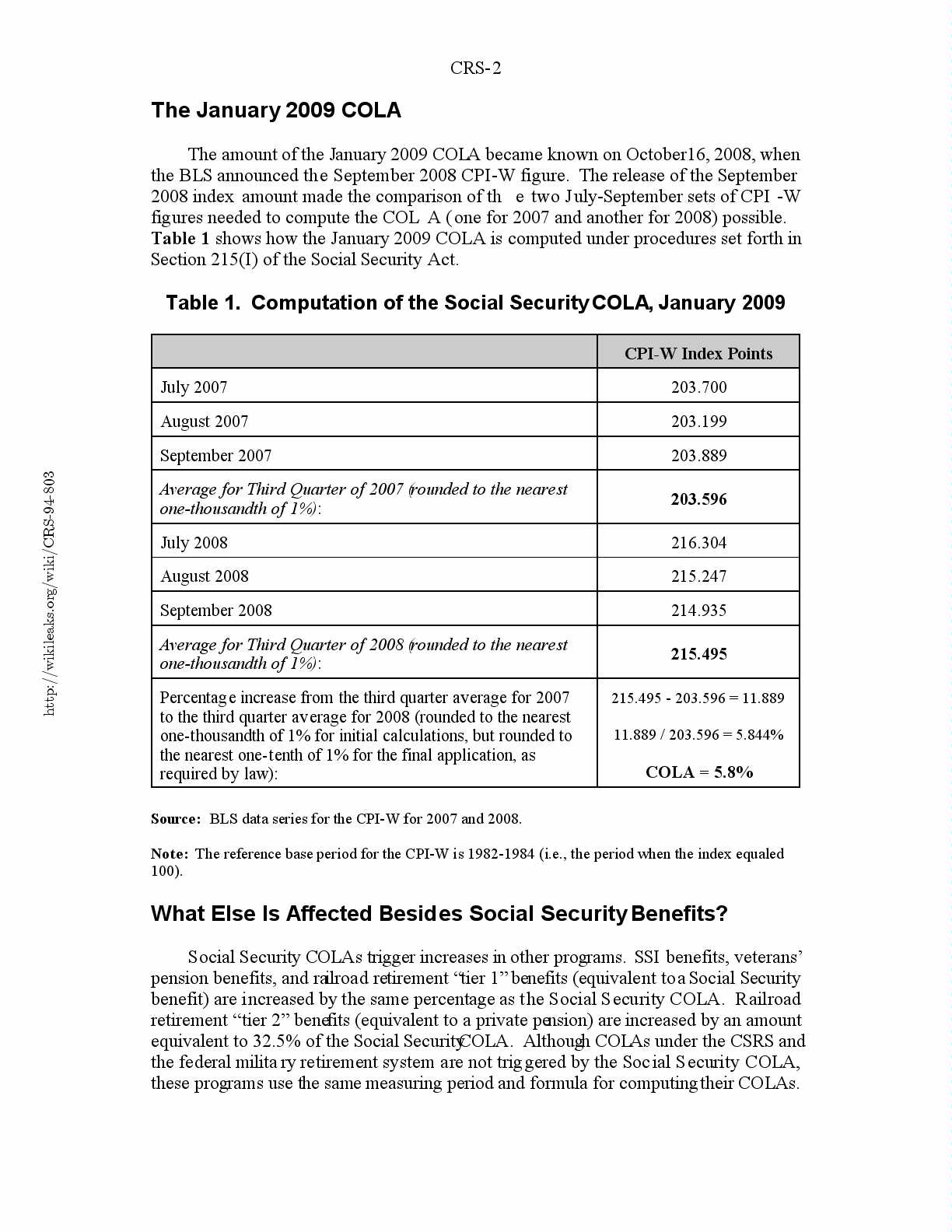

The January 2009 COLA

The amount of the January 2009 COLA became known on October 16, 2008, when

the BLS announced the September 2008 CPI-W figure. The release of the September

2008 index amount made the comparison of the two July-September sets of CPI-W

figures needed to compute the COLA (one for 2007 and another for 2008) possible.

Table 1 shows how the January 2009 COLA is computed under procedures set forth in

Section 215(I) of the Social Security Act.

Table 1. Computation of the Social Security COLA, January 2009

CPI-W Index Points

July 2007203.700

August 2007203.199

September 2007203.889

Average for Third Quarter of 2007 (rounded to the nearest203.596

one-thousandth of 1%):

July 2008216.304

August 2008215.247

September 2008214.935

Average for Third Quarter of 2008 (rounded to the nearest215.495

one-thousandth of 1%):

Percentage increase from the third quarter average for 2007215.495 - 203.596 = 11.889

to the third quarter average for 2008 (rounded to the nearest

one-thousandth of 1% for initial calculations, but rounded to11.889 / 203.596 = 5.844%

the nearest one-tenth of 1% for the final application, as

required by law):COLA = 5.8%

Source: BLS data series for the CPI-W for 2007 and 2008.

Note: The reference base period for the CPI-W is 1982-1984 (i.e., the period when the index equaled

100).

What Else Is Affected Besides Social Security Benefits?

Social Security COLAs trigger increases in other programs. SSI benefits, veterans’

pension benefits, and railroad retirement “tier 1” benefits (equivalent to a Social Security

benefit) are increased by the same percentage as the Social Security COLA. Railroad

retirement “tier 2” benefits (equivalent to a private pension) are increased by an amount

equivalent to 32.5% of the Social Security COLA. Although COLAs under the CSRS and

the federal military retirement system are not triggered by the Social Security COLA,

these programs use the same measuring period and formula for computing their COLAs.

View Page Image

Their recipients also receive a 5.8% COLA in January 2009.1 The COLA also triggers

other changes in the Social Security program, including the following items indexed to

the increase in national average wages:

!Taxable Earnings Base. The Social Security (or Old-Age, Survivors, and

Disability Insurance — OASDI) taxable earnings base (the maximum

amount of annual earnings subject to Social Security payroll taxes) will

increase to $106,800 in 2009 (from $102,000 in 2008).

!Exempt Amounts Under the Social Security Earnings Test. The exempt

amount under the earnings test is the maximum amount of earnings

allowed before a Social Security recipient’s benefits are affected. In

2009, for persons who are below the full retirement age (FRA) and will

not reach the FRA during that year, the annual exempt amount is $14,160

(up from $13,560 in 2008). There is a withholding of $1 of benefits for

every $2 of earnings above this exempt amount. The earnings test no

longer applies beginning with the month a recipient reaches the FRA.

During the calendar year in which a recipient reaches the FRA, a higher

exempt amount applies for those months preceding the individual’s

attainment of the FRA. In 2009, for persons who will reach the FRA in

that year, the annual exempt amount is $37,680, or $3,140 per month (up

from $36,120, or $3,010 per month, in 2008). There is a withholding of

$1 of benefits for every $3 of earnings above this exempt amount.

Although not triggered by the COLA, other changes are tied to the increase in

national average wages. In 2009, the amount of earnings needed for a Social Security

“quarter-of-coverage” is $1,090 (up from $1,050 in 2008). The monthly substantial

gainful activity amount for the non-blind disabled is $980 (up from $940 in 2008), and

the amount for the blind disabled is $1,640 (up from $1,570 in 2008). The annual

coverage thresholds for domestic workers and election workers increase by $100 from

2008 levels, to $1,700 and $1,500, respectively.

Table 2. History of Social Security Benefit Increases

Date Increase Was PaidAmount of Increase (shown as a percentage)

January 20095.8

January 20082.3

January 20073.3

January 20064.1

January 20052.7

January 20042.1

January 20031.4

January 20022.6

January 20013.5

January 20002.5a

January 19991.3

January 19982.1

January 19972.9

January 19962.6

January 19952.8

January 19942.6

January 19933.0

January 19923.7

January 19915.4

January 19904.7

January 19894.0

January 19884.2

January 19871.3

January 19863.1

January 19853.5

January 19843.5

July 19827.4

July 198111.2

July 198014.3

July 19799.9

July 19786.5

July 19775.9

July 19766.4b

July 19758.0

April/July 1974c11.0

October 197220.0

February 197110.0

February 197015.0

March 196813.0

February 19657.0

February 19597.0

October 195413.0

October 195212.5

October 1950 77.0

Source: Social Security Administration.

a. Originally computed as 2.4%, the COLA payable in January 2000 was

corrected to 2.5% under P.L. 106-554.

b. Automatic COLAs began.

c. Increase came in two steps.

View Page Image

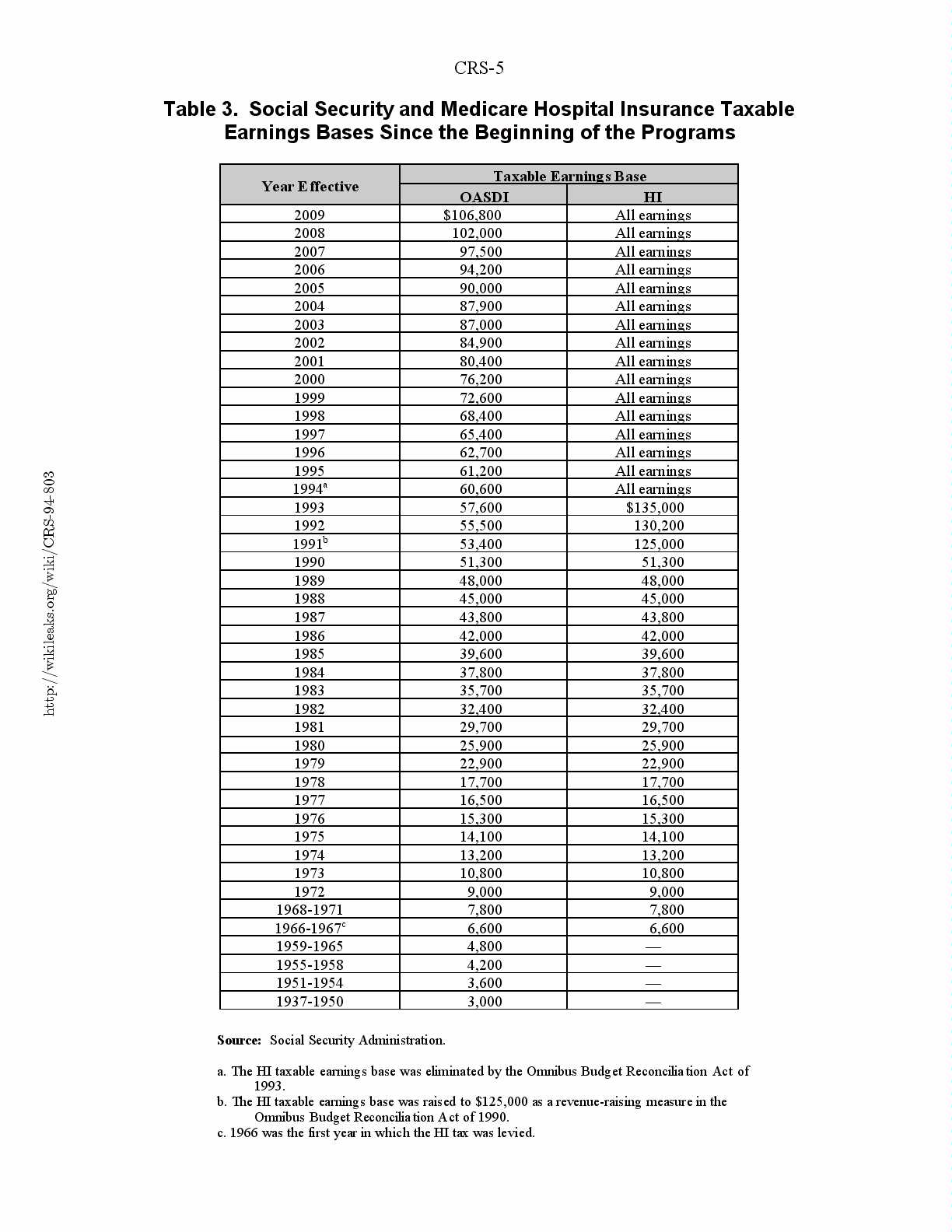

Table 3. Social Security and Medicare Hospital Insurance Taxable

Earnings Bases Since the Beginning of the Programs

Year EffectiveTaxable Earnings BaseOASDIHI

2009$106,800All earnings

2008102,000All earnings

200797,500All earnings

200694,200All earnings

200590,000All earnings

200487,900All earnings

200387,000All earnings

200284,900All earnings

200180,400All earnings

200076,200All earnings

199972,600All earnings

199868,400All earnings

199765,400All earnings

199662,700All earnings

199561,200All earningsa

199460,600All earnings

1993 57,600 $135,000

1992 55,500130,200b

1991 53,400 125,000

1990 51,300 51,300

1989 48,000 48,000

1988 45,000 45,000

1987 43,800 43,800

1986 42,000 42,000

1985 39,600 39,600

1984 37,800 37,800

1983 35,700 35,700

1982 32,400 32,400

1981 29,700 29,700

1980 25,900 25,900

1979 22,900 22,900

1978 17,700 17,700

1977 16,500 16,500

1976 15,300 15,300

1975 14,100 14,100

1974 13,200 13,200

1973 10,800 10,800

1972 9,000 9,000

1968-1971 7,800 7,800c

1966-1967 6,600 6,600

1959-19654,800 —

1955-19584,200 —

1951-19543,600 —

1937-19503,000 —

Source: Social Security Administration.

a. The HI taxable earnings base was eliminated by the Omnibus Budget Reconciliation Act of

1993.

b. The HI taxable earnings base was raised to $125,000 as a revenue-raising measure in the

Omnibus Budget Reconciliation Act of 1990.

c. 1966 was the first year in which the HI tax was levied.

View Page Image

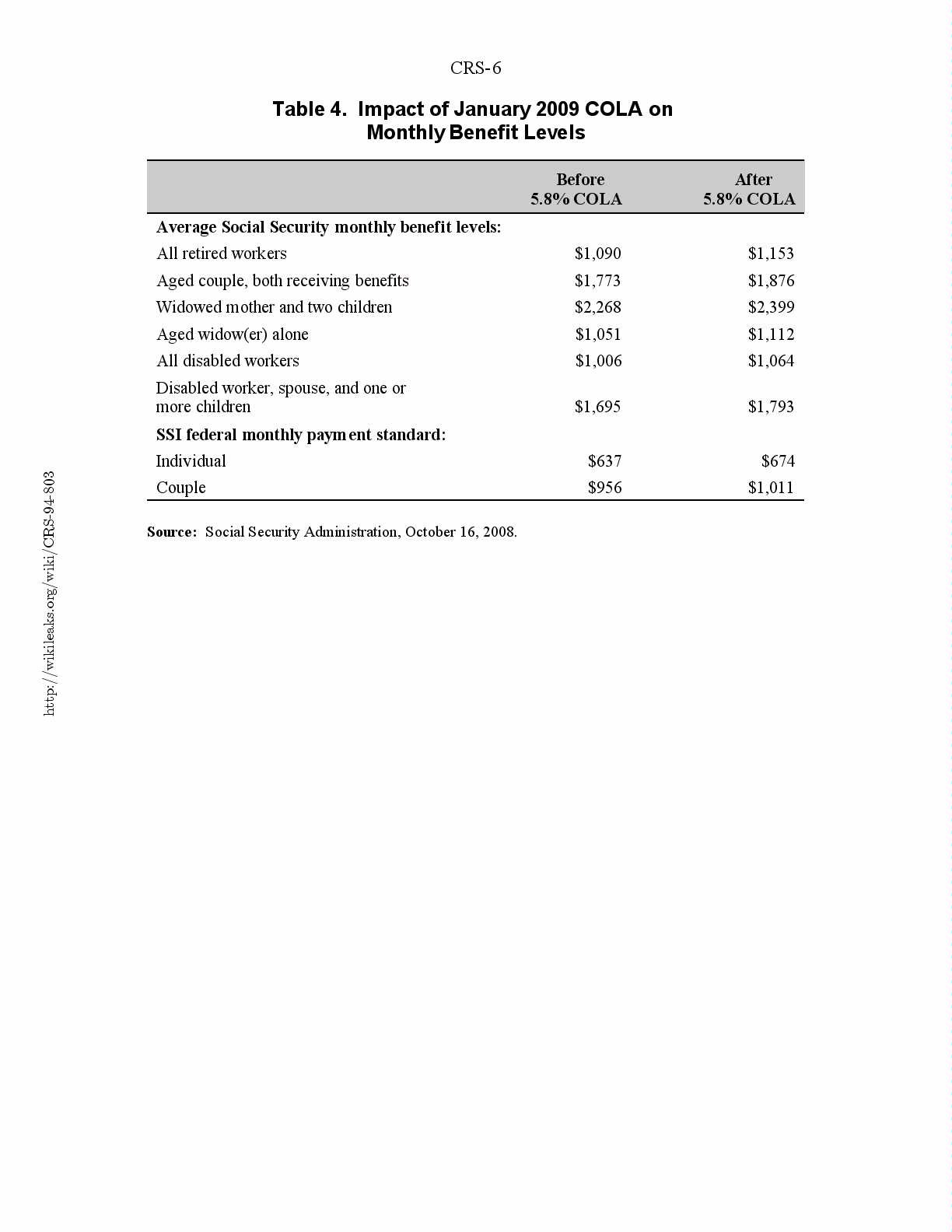

Table 4. Impact of January 2009 COLA on

Monthly Benefit Levels

Before After

5.8% COLA5.8% COLA

Average Social Security monthly benefit levels:

All retired workers$1,090$1,153

Aged couple, both receiving benefits$1,773$1,876

Widowed mother and two children$2,268$2,399

Aged widow(er) alone$1,051$1,112

All disabled workers$1,006$1,064

Disabled worker, spouse, and one or

more children$1,695$1,793

SSI federal monthly payment standard:

Indivi dual $637 $674

Couple $956 $1,011

Source: Social Security Administration, October 16, 2008.

View Page Image

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}